Workshops & Case Studies

Explore our latest workshops, case studies, and collaborative initiatives in quantitative finance. We regulary update our

offerings to reflect the latest developments and opportunities in the industry. Can't find what you're looking for?

Feel free to contact us – we're here to help!

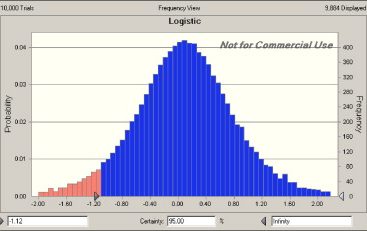

Value at Risk (VaR)

We focus on quantifying portfolio risk by applying historical simulation, variance–covariance, and Monte Carlo methods. Using Excel, Python, Bloomberg and LSEG Workspace, we estimate potential losses under normal and stressed

market conditions.

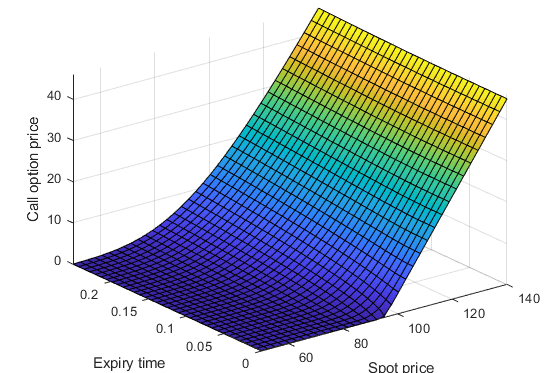

Option Valuation

We explore how to price options by applying Black–Scholes, binomial trees, and volatility

surfaces. We amodels in Excel and

Python and validate them with real-time data

from Bloomberg and LSEG Workspace.

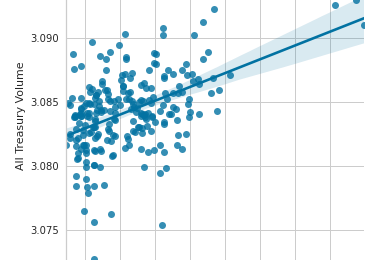

Financial Statistics

We strengthen our toolkit with regression analysis, time-series modeling, and hypothesis testing

tailored to financial markets. We work hands-on with real datasets from professional platforms

to extract signals and detect anomalies.

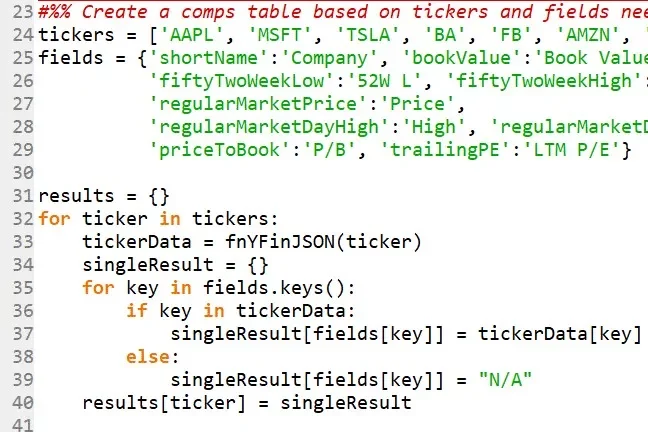

Python for Finance

We use Python to automate data extraction,

backtest strategies, and build analytics

dashboards. We connect APIs from

Bloomberg, LSEG and more to turn

raw market data into actionable insights.

Derivatives

We focus on pricing and hedging swaps,

futures, and structured products by applying

no-arbitrage principles and stochastic models.

We link theory to practice through case studies built on live curves and volatility surfaces.

Fixed Income Trading

We analyze yield curves, spreads, and credit risk to understand how bonds and rate products are priced and traded. We use Excel, Python, and professional data terminals to construct, value, and manage fixed income portfolios.